Reserve Bank of India (RBI) RBI is the central and regulatory bank for the Indian banking system. It was established in 1935. It has crucially important functions in formulating and enforcing the monetary policy of the country and controlling inflation. This institution acts as banker to the government and supervises the sound working of the banking system. Some of the main functions of RBI are:

- It regulates the issue and supply of the Indian rupee so that adequate liquidity prevails in the economy.

- It manages foreign exchange reserves to maintain stability in the exchange rates and the balance of payments.

- The central bank controls inflation by changing interest rates and by monitoring the monetary policy framework of the country.

About the Reserve Bank of India (RBI)

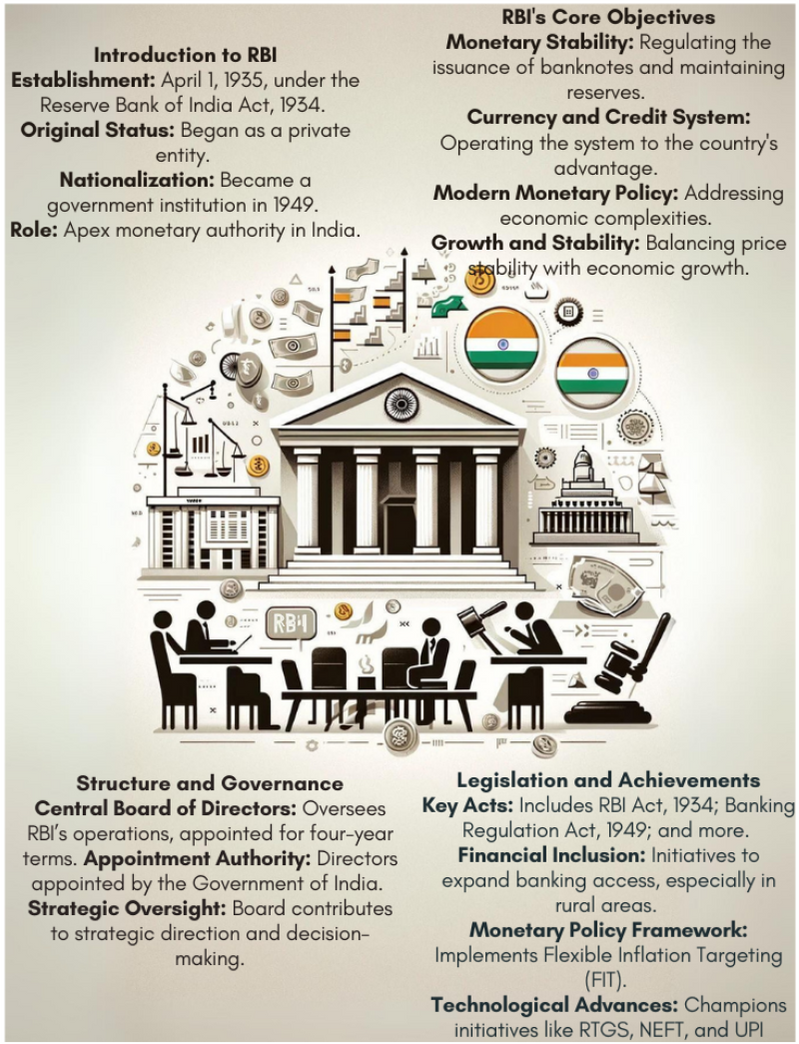

The Reserve Bank of India (RBI) stands as the apex monetary authority in India, playing a pivotal role in shaping the nation’s financial landscape. Established on April 1, 1935, by the provisions of the Reserve Bank of India Act, 1934, the RBI originally functioned as a private entity before being nationalized in 1949.

Objectives

The preamble of the RBI outlines its fundamental objectives, which include:

- Regulating the issuance of banknotes and maintaining reserves to uphold monetary stability.

- Operating the currency and credit system of the country to its advantage.

- Establishing a modern monetary policy framework to address the complexities of an evolving economy.

- Maintaining price stability while fostering economic growth.

Structure of RBI

The governance of the Reserve Bank is overseen by a central board of directors, appointed by the Government of India in accordance with the Reserve Bank of India Act. Directors serve a term of four years, contributing to the strategic direction and decision-making processes of the institution.

Acts Administered by the RBI

The Reserve Bank of India administers several key legislations to regulate and supervise various aspects of the financial system, including but not limited to:

- Reserve Bank of India Act, 1934

- Public Debt Act, 1944/Government Securities Act, 2006

- Government Securities Regulations, 2007

- Banking Regulation Act, 1949

- Foreign Exchange Management Act, 1999

- Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (Chapter II)

- Credit Information Companies (Regulation) Act, 2005

- Payment and Settlement Systems Act, 2007

- Factoring Regulation Act, 2011

These legislative frameworks empower the RBI to effectively regulate, supervise, and facilitate the smooth functioning of India’s financial ecosystem, ensuring stability, integrity, and growth.

Key Achievements of the Reserve Bank of India (RBI)

The Reserve Bank of India (RBI) has achieved significant milestones, including stabilizing inflation, managing foreign exchange reserves, promoting financial inclusion, and ensuring the smooth operation of India’s banking and monetary systems.

Monetary Stability Sustenance

The Reserve Bank of India is mandated by the Reserve Bank of India Act of 1934 to operate a contemporary monetary policy framework. Embracing flexibility, the RBI adopts Flexible Inflation Targeting (FIT) as its monetary policy framework. Every five years, in consultation with the Government of India, the RBI sets inflation targets based on the Consumer Price Index (CPI).

Robust Financial Sector Regulation

The RBI implements a suite of measures aimed at fortifying the banking sector and bolstering financial stability. Through regular reviews and updates of banking regulations, it ensures the resilience of financial institutions. Notably, the introduction of the Prompt Corrective Action (PCA) framework is a strategic move to address Non-Performing Assets (NPAs) and uphold the solvency of banks.

Effective Public Debt Management

Skillfully managing public debt, the Reserve Bank facilitates government borrowing at favorable interest rates. By orchestrating loans for the government and extending short-term advances, the RBI plays a pivotal role in financing public sector expansion, thereby contributing to economic growth.

Advancement of Financial Inclusion

The RBI spearheads initiatives to promote financial inclusion and broaden access to banking services, particularly in rural and remote areas. Branch licensing guidelines, priority sector lending norms, and the establishment of payment banks and small finance banks have significantly expanded the accessibility of formal banking services to previously underserved demographics.

Proficient Foreign Exchange Management

Under the ambit of the Foreign Exchange Management Act of 1999, the RBI adeptly manages all foreign exchange operations. Intervening in the foreign exchange market to curb excessive volatility and uphold external sector stability, the RBI’s stewardship has fostered confidence in India’s robust foreign exchange reserves.

Modernization of Payment and Settlement Systems

Proactively modernizing payment and settlement systems, the RBI facilitates efficient and secure transactions. Initiatives such as Real-Time Gross Settlement (RTGS), National Electronic Funds Transfer (NEFT), and Unified Payments Interface (UPI) have revolutionized the landscape, ensuring swift and seamless transactions.

Embracing Technological Innovations

Championing technological advancements in banking and finance, the RBI advocates for digital banking, electronic payments, and fintech innovations. This embrace of technology enhances efficiency and inclusivity in the financial sector, aligning with global trends and fostering economic growth.

Enhanced Regulation of Non-Banking Financial Companies (NBFCs)

Recognizing the growing significance of NBFCs in India’s financial ecosystem, the RBI enforces stringent regulations to bolster their resilience and mitigate systemic risks. Guidelines for asset-liability management, capital adequacy, and corporate governance fortify the sector’s stability.

Supporting Economic Development

Through its monetary policy interventions and developmental initiatives, the RBI catalyzes economic growth, fosters employment generation, and nurtures overall economic development. The establishment of a robust structure of Development Banking and specialized financial institutions underscores its commitment to sustainable progress.

Boosting Public Confidence in the Banking Sector

The RBI undertakes measures to bolster public confidence in the banking system. Rigorous supervision of Scheduled Commercial banks averts failures, while the Deposit Insurance and Credit Guarantee System safeguards depositors’ interests, instilling trust and stability in the banking sector.

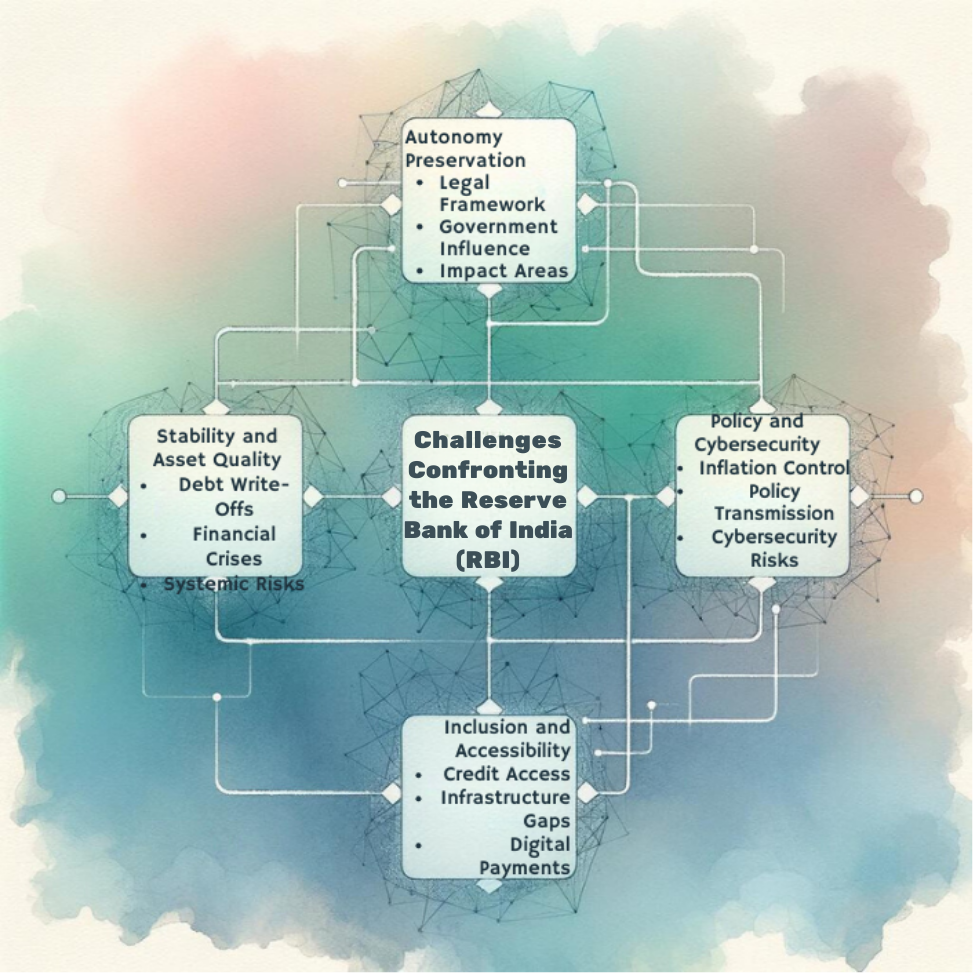

Challenges Confronting the Reserve Bank of India (RBI)

The Reserve Bank of India (RBI) faces challenges like controlling inflation, managing fluctuating exchange rates, addressing financial sector reforms, and navigating global economic uncertainties while ensuring stability in India’s monetary and banking systems.

Preservation of Autonomy

While the Reserve Bank of India Act delineates the RBI’s operational framework, Section 7 grants the central government authority to issue directives deemed necessary in the public interest, subject to consultation with the Governor of the Bank. The absence of a legal mandate for RBI’s autonomy has led to instances where governmental influence encroached upon the central bank’s decision-making, particularly in matters related to monetary policy, regulatory actions, and reserve utilization.

Inflation Control Dilemmas

Despite the implementation of a flexible inflation-targeting framework, the RBI grapples with the challenge of taming inflationary pressures. Data from the National Statistical Office reveals a notable uptick in the food basket’s inflation rate, a significant component of the Consumer Price Index. India’s intricate economic structure, coupled with supply-side constraints and external factors like fluctuating oil prices, pose formidable hurdles in achieving the desired inflation target, complicating the RBI’s pursuit of price stability.

Debt Write-Off Concerns

The significant write-off of loans has facilitated a decline in Gross Non-performing Assets (GNPA) to a decade-low level by March 2023. However, the practice of writing off loans without diligent recovery endeavors raises apprehensions regarding the transparency and reliability of financial reporting. While ostensibly improving short-term balance sheets, this approach fails to address the root causes of Non-Performing Assets (NPAs), casting doubts on the effectiveness of corrective measures.

Financial Stability Imperatives

Safeguarding financial stability and mitigating systemic risks remain ongoing challenges for the RBI. Factors such as rapid credit expansion, interconnectivity among financial institutions, and vulnerabilities in sectors like shadow banking underscore the complexities of ensuring a resilient financial system. Recent episodes involving financial crises in entities like YES Bank and Infrastructure Leasing & Financial Services Ltd underscore the imperative for enhanced oversight mechanisms to preempt systemic disruptions.

Monetary Policy Transmission Gaps

The incomplete transmission of monetary policy actions poses a persistent challenge for the RBI. Despite cumulative policy rate cuts, the translation into corresponding reductions in lending rates by banks remains suboptimal. Factors such as institutional rigidities, liquidity conditions, and risk perceptions impede the efficacy of monetary policy transmission, highlighting the need for systemic reforms to enhance the efficacy of policy measures.

Cybersecurity in the Digital Age

The rapid proliferation of digital banking and financial technologies outpaces regulatory frameworks, posing challenges in ensuring compliance with evolving cybersecurity standards and data protection regulations. Incidents such as the recent Paytm crisis underscore the vulnerabilities inherent in digital financial ecosystems, necessitating robust cybersecurity measures to safeguard financial integrity and consumer trust.

Financial Inclusion and Credit Accessibility Hurdles

Despite commendable efforts to promote financial inclusion, ensuring equitable access to credit remains a formidable challenge, particularly for marginalized borrowers. Rural areas often grapple with insufficient banking infrastructure and limited internet connectivity, hindering access to financial services. The projected exponential growth of India’s digital payments market underscores the urgency of addressing these disparities to foster inclusive economic growth.

Strategies for Enhancing Reserve Bank of India (RBI) Operations

Enhancing Reserve Bank of India (RBI) operations requires adopting advanced technology, improving regulatory frameworks, promoting financial inclusion, and strengthening risk management practices to ensure effective monetary policy and financial stability in a dynamic global economy.

Fortifying Regulatory Frameworks

Augment regulatory frameworks to ensure vigilant supervision and regulation of banks and financial institutions, incorporating periodic reviews and updates to adapt to evolving market dynamics and emerging risks. The establishment of the Financial Stability and Development Council (FSDC) as proposed by the Raghuram Rajan committee in 2008 underscores the imperative of bolstering financial stability and coordination among regulators

Advancing Financial Inclusion Initiatives

Deploy measures to expand financial inclusion, encompassing initiatives to broaden access to banking services, promote digital payments, and facilitate outreach to underserved populations and regions. The phased approach advocated by the Nachiket Mor Committee in 2014 towards universal financial inclusion underscores the importance of innovative delivery mechanisms.

Streamlining Monetary Policy Transmission

Rectify bottlenecks in monetary policy transmission mechanisms to ensure that policy rate adjustments effectively influence lending and borrowing rates across the financial spectrum, stimulating credit flow to vital sectors of the economy. Measures such as the adoption of the Marginal Cost of Funds based Lending Rate (MCLR) have been instrumental in enhancing policy rate transmission efficacy.

Reinforcing Risk Management Protocols

Reinforce risk management frameworks within banks and financial institutions to proactively identify, evaluate, and mitigate diverse risks, including credit, liquidity, operational, and cyber risks. Initiatives like the Insolvency and Bankruptcy Code (IBC) framework have facilitated the resolution of issues such as non-performing assets, fostering a conducive environment for robust credit growth.

Promoting Technological Innovations

Foster a culture of technological innovation and integration within the financial landscape, encompassing the adoption of fintech solutions, digital banking services, and blockchain technology, while prioritizing data security and consumer protection. The establishment of the Regulatory Sandbox (RS) ecosystem by the RBI in August 2019 exemplifies efforts to systematically nurture the fintech ecosystem

Enhancing Transparency and Communication Channels

Amplify transparency and communication channels between the RBI, financial institutions, and the public to enhance comprehension of monetary policy decisions, regulatory reforms, and the overarching functioning of the central bank. Platforms such as the RBI Governor’s bi-monthly monetary policy statements and press conferences serve as conduits for elucidating policy rationale and future outlooks.

Capacity Building and Skill Enhancement

Invest in comprehensive capacity-building and training initiatives for RBI personnel and stakeholders to augment proficiency, expertise, and competency in areas like financial regulation, supervision, monetary policy formulation, and emerging technologies. Recommendations from committees like the Damodaran Committee in 2011 advocate for enhanced training programs to elevate service standards and customer satisfaction within banks.

Strengthening Governance Mechanisms

Implement measures to fortify governance structures, accountability frameworks, and internal controls within the RBI to facilitate informed decision-making, transparency, and operational integrity. The directives outlined by committees such as the P.J. Nayak Committee in 2014 emphasize the enhancement of autonomy and governance within public sector banks to optimize efficiency and accountability

Fostering Collaborative Partnerships

Nurture collaborative partnerships with regulatory bodies, governmental entities, international organizations, and stakeholders to address cross-cutting issues, foster financial stability, and realize shared objectives. Active participation in global forums such as the Financial Stability Board (FSB) and the Bank for International Settlements (BIS) underscores the RBI’s commitment to international cooperation and policy coordination

Conclusion

As the Reserve Bank of India commemorates ninety years of its existence, it stands as a beacon of stability, resilience, and progress in India’s economic landscape. From its humble beginnings to its current stature as a formidable central bank, the RBI’s journey is replete with accomplishments, challenges, and invaluable contributions to the nation’s growth story. As India marches forward into a new era of economic dynamism, the RBI remains steadfast in its commitment to serving the nation and shaping its destiny.

| Reserve Bank Of India UPSC Notes |

| 1. Reserve Bank of India (RBI) was established in 1935 under the Reserve Bank of India Act to regulate India’s financial system and monetary policy. 2. The RBI is responsible for maintaining price stability, ensuring adequate money supply, and promoting economic growth while managing inflation and exchange rates. 3. It plays a key role in issuing currency, managing foreign exchange reserves, and maintaining the stability of the rupee. 4. The RBI regulates and supervises the banking sector, ensuring the health and stability of banks and financial institutions. 5. The central bank implements monetary policy tools like repo rates, reverse repo rates, and open market operations to control inflation and liquidity in the economy. 6. RBI manages public debt and acts as the banker to the government, conducting auctions for government securities and managing fiscal deficits. 7. The central bank is also responsible for the regulation of payment and settlement systems, ensuring secure and efficient financial transactions. 8. The RBI plays a crucial role in financial inclusion by promoting access to banking services for underserved and rural populations, including through initiatives like priority sector lending. |